Forecasting made Simple and Transparent

From politicians and businesses to unions and individuals, many stakeholders are closely watching how economic conditions are likely to unfold in the future. While forecasts for key economic indicators such as growth and inflation can easily be obtained, it is often unclear how large the uncertainty behind common estimates is. As now illustrated by scientists from the Karlsruhe Institute of Technology (KIT) and the Heidelberg Institute for Theoretical Studies (HITS) in the “Annals of Applied Statistics”, a simple method can be used to address this problem.

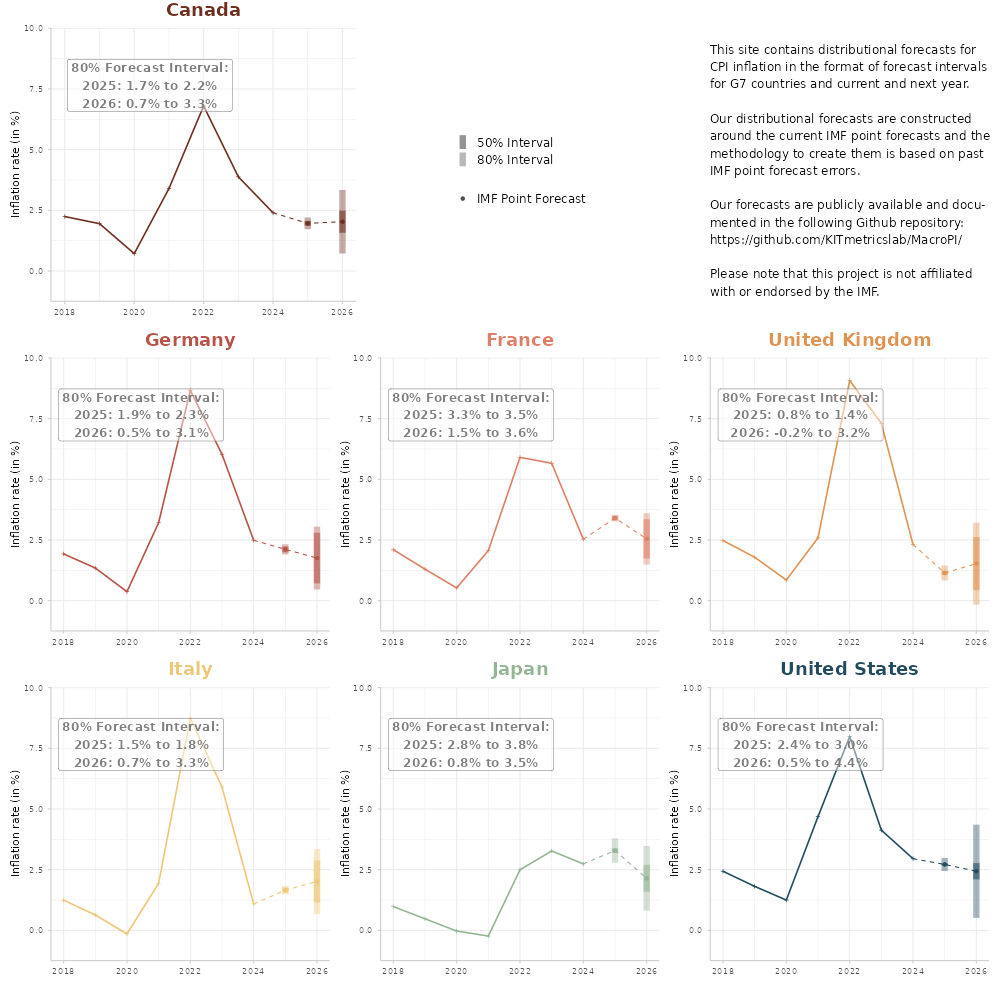

The team developed a method for predicting the uncertainty of forecasts for economic growth and inflation in the G7 countries. The uncertainty is communicated in the format of forecast intervals, yielding statements such as “With 80% probability, inflation in Germany in 2026 will be between 0.5% and 3%”. The method to obtain these forecast intervals is based on point forecasts published by the International Monetary Fund (IMF), paired with a statistical analysis of the IMF’s recent forecast errors. While significantly less complex, the combined method yields interval forecasts that perform similarly to, or even better than, classical reference methods.

Transparent and easily applicable

“The reference methods use advanced time series models that are difficult to estimate from limited macroeconomic data,” says Friederike Becker, research associate in the Institute of Statistics at KIT and first author of the study. “In contrast, the new method leverages the economic expertise at the IMF, and uses a transparent and easily applicable way to quantify the underlying uncertainty,” adds Melanie Schienle, professor of Statistics and Econometrics at KIT and senior researcher in the Computational Statistics group at HITS.

The procedure can be employed for all types of point forecasts, provided an informative history of recent forecast errors is available, from which to estimate the distribution of forecast errors. In addition to the method being interpretable, transparent and cost-efficient to implement, this versatility makes it user-friendly, even for non-experts.

The recently published work analyzes this method on past data – in addition to this, the scientists make their forecasts publicly available in real time and provide an easy-to-use website with graphical illustrations of their interval forecasts.

Publication:

Friederike Becker, Fabian Krüger, Melanie Schienle. Simple Macroeconomic Forecast Distributions for the G7 Economies. Ann. Appl. Stat. 19(4): 2878-2897.

https://doi.org/10.1214/25-AOAS2095

Scientific Contact:

Prof. Dr. Melanie Schienle

Chair of Statistics and Econometrics, Institute of Statistics, KIT

melanie schienle@kit edu

Media contact:

Angela Michel

Head of Communications

Heidelberg Institute for Theoretical Studies (HITS)

E-Mail: angela.michel@h-its.org

www.h-its.org

Dr. Joachim Hoffmann

Karlsruher Institut für Technologie (KIT)

E-Mail: joachim.hoffmann@kit.edu

www.kit.edu

About HITS

HITS, the Heidelberg Institute for Theoretical Studies, was established in 2010 by physicist and SAP co-founder Klaus Tschira (1940-2015) and the Klaus Tschira Foundation as a private, non-profit research institute. HITS conducts basic research in the natural, mathematical, and computer sciences. Major research directions include complex simulations across scales, making sense of data, and enabling science via computational research. Application areas range from molecular biology to astrophysics. An essential characteristic of the Institute is interdisciplinarity, implemented in numerous cross-group and cross-disciplinary projects. The base funding of HITS is provided by the Klaus Tschira Foundation.